Stock in Focus: Superloop

Who are they and what do they do?

Superloop (SLC) is an Australian telecommunications company that provides internet and connectivity services to consumer, business and wholesale customers. The company is a key enabler in the shift away from incumbent providers like Telstra, both through its direct-to-consumer plans as well as its white-labelled offerings to wholesale customers. The trend away from major telco incumbents has seen market share from the three largest players reduce from 79% in 2023 to 67% today1, with SLC a key beneficiary of this move.

What are our 3 key drivers for the company?

- Consumer Subscriber Growth: SLC has been very successful in growing its consumer facing brand, taking significant share from incumbent providers. The company offers a much more attractive price point than the incumbents without compromising service. This value proposition has played out in subscriber numbers, which are up more than 2x over 3 years.

- Wholesale Subscriber Growth: SLC has participated in the disruption of incumbent internet service providers through the enablement of other challengers through its white-labelled offering. Key to growth has been in its contract with Origin Energy, which has almost doubled its subscriber base in two years and has ambitions to more than double that again. SLC takes a fixed fee on this offering irrespective of Origin’s retail pricing, meaning if Origin aggressively chases subscriber growth it does not impact the economics of SLC’s offering.

- Margin Expansion: With a significant fibre network and a disruptor mindset, the company has been very effective in utilising new technologies such as AI to minimise its cost growth and deliver compelling operating leverage over its recent history. We see this trend continuing, as the incremental costs per new subscriber from here onwards are relatively modest.

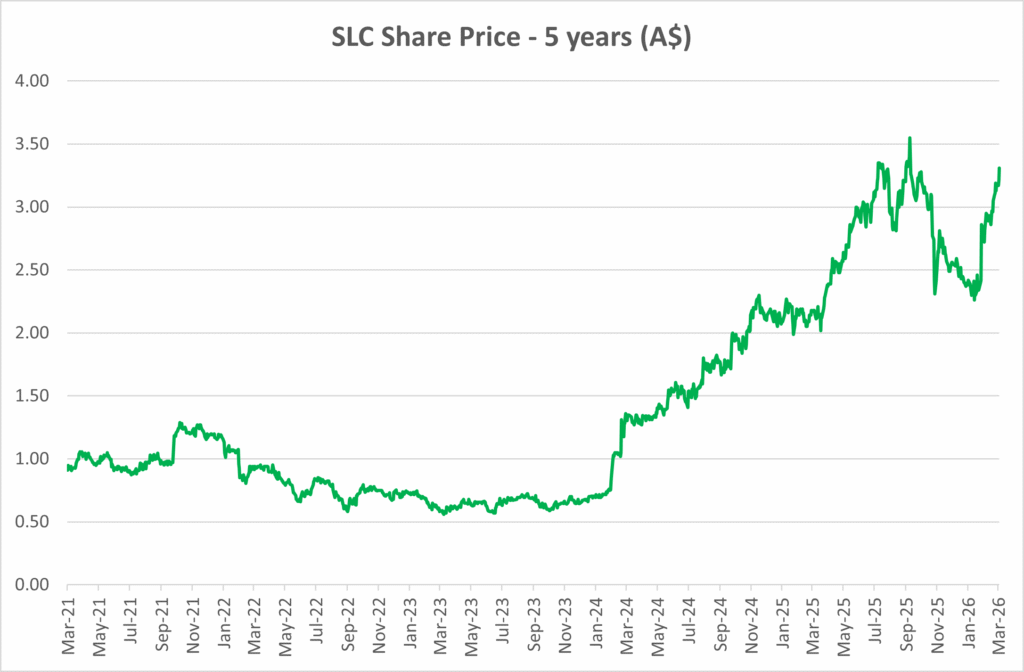

What do we think the company is worth?

Lennox’s valuation is typically based on a combination of our year-3 earnings forecast for the company, coupled with the PE premium/discount we believe the business should trade on. Superloop is currently trading on an FY29 PE of 15x and forecast to deliver material FCF over the next 3-years*. On that basis we believe SLC could be worth more than $4 by FY292.

1NBN Wholesale Market Indicators Report, Dec-22 & Dec-25

2Lennox Capital Partners forecasts, Mar-26.

*Current Price as at 30 March 2026: $3.21 AUD

This material has been prepared by Lennox Capital Partners Pty Ltd ABN 19617001966 AFSL 498737 (Lennox). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information.

Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon.

Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed.