Stock in Focus: FDC Holdings

Source: FDC Consolidated Holdings Prospectus, Jun-26

Who are they and what do they do?

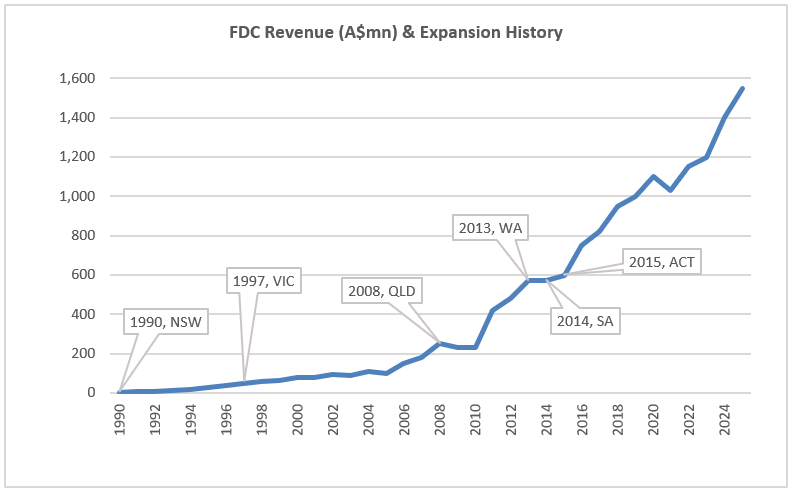

FDC is one of Australia’s largest national construction, fitout and refurbishment businesses. Founded in 1990, FDC employs over 700 staff and generated group revenue of around A$1.5 billion in FY25. The business prides itself on being relationship-driven, with a broad and diversified customer base and a “Made Personal” delivery culture that has earned 140+ Master Builders Association awards.

What are our 3 key drivers for the company?

- Geographic expansion driving revenue growth: FDC originated in NSW and has built a very strong presence in that market. Victoria and Queensland operations have gained reasonable scale but are still a fraction of NSW’s size, with other states (SA, WA, ACT) being smaller again. We believe the expected growth in non-NSW states over coming years will drive overall growth in FDC’s business over the medium term.

- Data centre tailwind: FDC is a recognised leader in mission-critical data-centre delivery, having built facilities for major banks, large colocation operators, and well-known data centre clients. The structural surge in AI and cloud-driven demand is fuelling an unprecedented Australian datacentre construction pipeline, and FDC’s established track record offer the potential to capture a disproportionate share of this multi-year growth.

- Operating leverage: Three decades of growth have lifted FDC to roughly A$1.5bn in annual revenue with a reliable earnings margin. We believe ongoing growth and scale will provide the ability for FDC to improve margins due to ongoing gains in efficiency.

What do we think the company is worth?

Lennox’s valuation is typically based on a combination of our year-3 earnings forecast for the company, coupled with the PE premium/discount we believe the business should trade on. As FDC does not have a listed track record we apply a further discount to that target multiple. Taking the view that FDC will ‘earn their stripes’ in the listed market over coming years, we believe the business should trade on a market multiple which, combined with our internal earnings forecasts for the business delivers a medium-term valuation of more than $4 (versus the IPO price of $3.00). The company also intends to payout 80% of profits as dividends, meaning a 6.5% FY27 dividend yield.